Introduction

The Securities Exchange Board of India (“SEBI”) introduced the concept of a Social Stock Exchange (as defined below) on July 25, 2022, by amending the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (“ICDR Regulations”), SEBI (Listing Obligations and Disclosure Requirements), Regulations, 2015 (“LODR Regulations”), and SEBI (Alternative Investment Fund) Regulations, 2012 (“AIF Regulations”).

In furtherance to the above, on September 19, 2022, SEBI vide Circular No. SEBI/HO/CFD/PoD-1/P/CIR/2022/120, introduced a detailed framework on SSE. The framework provides for the minimum requirements to be followed by a not-for-profit organization intending to list/register on the SSE, disclosure requirements, and the disclosure of annual impact report by all social enterprises. Chapter X-A of the ICDR Regulations lays down the listing requirements for an NGO seeking to list on the SSE.

The SSE platform is a path-breaking concept in India, as it allows Social Enterprises (as defined below) to access public capital by raising funds through institutional and non-institutional investors (however, SEBI may permit other classes of investors).[i] Through the SSE framework, SEBI has put into effect various transparency and disclosure requirements to ensure compliance of NPOs with laws and regulations.

Definitions:

Some of the key definitions are as follows:

(a)As per Regulations 292A(e)[ii], a Not-for-Profit Organization (“NPO”) means a Social Enterprise which is any of the following entities:

(i) a charitable trust registered under the Indian Trust Act, 1882;

(ii) a charitable trust registered under the public trust statute of the relevant state;

(iii) a charitable society registered under the Societies Registration Act, 1860;

(iv) a company incorporated under Section 8 of the Companies Act, 2013; and

(v) any other entity as may be specified by the Securities Exchange Board of India (“Board”).

(b) ‘Social Enterprise’ means either an NPO or a For-Profit Social Enterprise that meets the eligibility criteria specified under the ICDR Regulations.[iii]

(c) ‘Social Stock Exchange’ (“SSE”) is a separate segment of a recognized stock exchange permitting registration of an NPO and/or list of the securities issued by an NPO through their nationwide trading terminals.[iv]

(d) A ‘For-Profit Social Enterprise’ is a company or a body corporate operating for profit, it is a Social Enterprise for the purposes of ICDR Regulations, however, it does not include a company incorporated under Section 8 of the Companies Act, 2013.[v]

(e) ‘Social Auditor’ is an individual registered with a self-regulatory organization under the Institute of Chartered Accountants of India or such other agency, as may be specified by SEBI, who has qualified a certification program conducted by National Institute of Securities Market and holds a valid certificate[vi].

Therefore, from the aforementioned definitions, it is understood that an NPO and an FPSE, are broad classifications of a Social Enterprise. Furthermore, the use of the term ‘Social Enterprise’ shall mean an FPSE and/or NPO, however, the usage of the term ‘NPO’ shall strictly mean an NPO only.

Applicability of Chapter X-A of the ICDR Regulations:

The provisions of Chapter X-A are applicable to[vii]: (i) an NPO seeking to only get registered on the SSE, without the intention to raise funds; (ii) an NPO seeking to register and raise funds through the SSE; (iii) a For-Profit Social Enterprise (“FPSE”) desirous of being identified as a Social Enterprise under the ICDR Regulations.

Eligibility conditions to being identified as a Social Enterprise:

As evidenced by the definition, an NPO or a FPSE is a social enterprise, however for either to be identified as a Social Enterprise, the NPO or FPSE shall establish ‘primacy of its social intent.’[viii]

The ‘primacy of intent’ can be established upon the satisfaction of below eligibility criteria(s):

(a) the Social Enterprise shall be indulged in at least one of the following activities:

- eradicating hunger, poverty, malnutrition, and inequality;

- promoting health care including mental healthcare, sanitation and making available safe drinking water;

- promoting education, employability, and livelihoods;

- promoting gender equality, empowerment of women and LGBTQIA+ communities;

- ensuring environmental sustainability, addressing climate change including mitigation and adaptation, forest, and wildlife conservation;

- protection of national heritage, art, and culture;

- training to promote rural sports, nationally recognised sports, Paralympic sports, and Olympic sports;

- supporting incubators of Social Enterprises;

- supporting other platforms that strengthen the non-profit ecosystem in fundraising and capacity building;

- promoting livelihoods for rural and urban poor including enhancing income of small and marginal farmers and workers in the non-farm sector;

- slum area development, affordable housing, and other interventions to build sustainable and resilient cities;

- disaster management, including relief, rehabilitation, and reconstruction activities;

- promotion of financial inclusion;

- facilitating access to land and property assets for disadvantaged communities;

- bridging the digital divide in internet and mobile phone access, addressing issues of misinformation and data protection;

- promoting welfare of migrants and displaced persons;

- any other area as identified by the Board or Government of India from time to time.

(b) the Social Enterprise shall target underserved or less privileged population segments or regions recording lower performance in the development priorities of central or state governments;

(c) the Social Enterprise shall have at least 67% of its activities, qualifying as eligible activities to the target population, to be established through one or more of the following:

- at least 67% of the immediately preceding 3-year average of revenues comes from providing eligible activities to members of the target population;

- at least 67% of the immediately preceding 3-year average of expenditure has been incurred for providing eligible activities to members of the target population;

- members of the target population to whom the eligible activities have been provided constitute at least 67% of the immediately preceding 3-year average of the total customer base and/or total number of beneficiaries.

Furthermore, if the NPO or FPSE is engaged as a corporate foundation, political or religious organization, as a professional or trade association, or as an infrastructure and housing company (except affordable housing), such NPO or FPSE, as the case may be, shall not be eligible to be identified as a Social Enterprise.[ix]

Registration of an NPO:

An NPO seeking to raise funds through the SSE shall mandatorily register itself with the SSE.[x]

Eligibility criteria to raise funds through SSE:

An NPO desirous of registration on SSE shall fulfil the following criteria, in accordance with Regulation 292F(1) of ICDR Regulations[xi]:

| Parameter | Compliance document | Details |

| Legal Requirements | ||

| The entity is registered as an NPO | Registration certificate valid at least for the next 12 months at the time of seeking registration with SSE | As per Regulation 292A(e) of ICDR Regulations |

| Ownership and control | Governing document (MoA & AoA/ Trust Deed/ Byelaws/ Constitution) | Disclose if NPO is owned and/or controlled by the government or private |

| Exemption under the Income Tax Act | Registration Certificate under section 12A/12AA/12AB under Income Tax Act, 1961 | Registration Certificate under section 12A/12AA/12AB to be valid for at least the next 12 months. Does not have a notice or ongoing scrutiny by Income Tax. |

| Registration with Income Tax as an NPO | Income Tax PAN | Valid IT PAN |

| Age of the NPO | Registration certificate | Minimum 3 years |

| Deduction under Income Tax Act, 1960 | Valid 80G registration under the Income Tax Act, 1961. | Entity to ensure whether tax deduction is available or not to investors. |

| Eligible to be a Social Enterprise | Requirements with Regulation 292E of ICDR Regulations | As may be specified by SSE |

| Minimum Fund Flows | ||

| Annual Spending in the past financial year | Receipts or Payments from Audited Accounts/ Fund Flow Statement | Must be at least Rs. 50 lakhs |

| Funding in the past financial year | Receipts from Audited accounts/ Fund Flow Statement | Must be at least Rs. 10 lakhs |

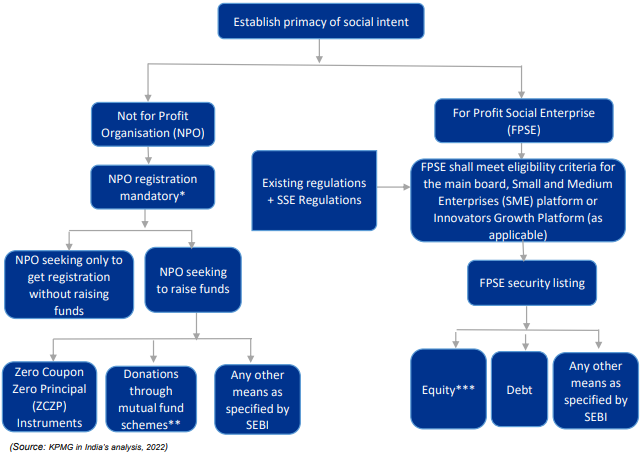

Methods for raising funds by an NPO or FPSE:

Below mentioned is a flowchart simplifying the steps available to a NPO or a FPSE, as the case may be, to raise funds upon registration with the SSE:

*An NPO registered with the SSE is required to comply with the regulations as laid down by SEBI.

**A registered NPO may raise funds from donations through mutual fund schemes as specified by SEBI.

*** An FPSE may raise funds through issuance of equity shares on the main board, SME platform or innovators growth platform or equity shares issued to an Alternative Investment Fund including a social impact fund.

Compliances by a Social Enterprise:

Chapter IX- A of the LODR Regulations lays down the obligations that an FPSE and an NGO have to fulfil to enable them to remain in compliance with law and raise funds through the SSE.

Primarily, the provisions of Chapter IX-A are applicable to an FPSE whose securities are listed on the SSE, and an NPO that is registered on the SSE.[xii]

A. In accordance with Regulation 91C of the LODR Regulations[xiii], an NPO registered on an SSE or a NPO which has raised funds on SSE, within 60 days from the end of the financial year, or a period as specified by SEBI, has to provide annual disclosures in detail on aspects as laid down below[xiv]:

- General aspects;

- Governance aspects; and

- Financial aspects.

B. A Social Enterprise whose designated securities are listed on the SSE, shall[xv]:

- shall frame a policy for determination of materiality, duly approved by its board or management, as the case may be, which shall be disclosed on the Social Stock Exchange(s);

- authorize one or more of its Key Managerial Personnel for the purpose of determining the materiality of an event or information and for the purpose of making disclosures under LODR Regulations to the SSE, and the contact details of such personnel shall also be disclosed to the SSE;

- shall disclose to the SSE within seven days from the occurrence of an event, which may have a material impact on the planned achievement of outputs or outcomes of the Social Enterprise, and the steps being taken by the Social Enterprise to address the same. Further, the Social Enterprise shall provide continual disclosures till the aforementioned event remains material;

- provide specific and adequate replies to all queries raised by SSE;

- suo motu confirm or deny any reported events or information to SSE;

- disclose on the website all such events or information as required to be disclosed to SSE.

C. Annual Impact Report: All Social Enterprise(s), who have registered and /or raising funds through SSE, shall:

- provide an audited Annual Impact Report (“AIR”) within 90 days from the end of the financial year;

- capture the qualitative and quantitative aspects of the social impact generated by the entity for which funds have been raised through SSE;

- cover an NPO’s significant activities, interventions, programs, or projects during the year and the methodology for determining such significance if the NPO is registered on SSE without listing any security;

- in a situation where the NPO / FPSE is a social impact fund (as defined under SEBI regulations), and the recipients of the funds are Social Enterprise(s) who have registered or are raising funds through SSE, such fund must disclose an overall AIR for the fund covering all organizations where its funds are deployed;

- ensure that the AIR, at minimum, covers aspects like strategic intent and planning, the approach, and the impact scorecard;

- have the AIR audited by a Social Auditor and the Social Enterprise(s) shall disclose the report of the Social Auditor along with the AIR.

D. An NPO listed on SSE shall submit a statement of the utilisation of funds within 45 days from the end of the quarter in the following manner[xvii]:

- category-wise amount of monies raised;

- category-wise amount of monies utilised;

- balance amount remaining utilised.

The contents of this note are limited to the concept of SSE in India, the primary listing requirement, and the annual disclosures of an NPO listed or registered with SSE. Furthermore, the SSE framework, read with ICDR Regulations and LODR Regulations provides different methods for raising funds and issuing securities which have been discussed in detail under various SEBI regulations.

[i] Regulation 292C, SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

[ii] Regulation 292A(e), SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

[iii] Regulation 292A(h), SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

[iv] Regulation 292A(i), SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

[v] Regulation 292A(c), SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

[vi] Regulation 292A(f), SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

[vii] Regulation 292B, SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

[viii] Regulation 292E(1), SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

[ix] Regulation 292E(3), SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

[x] Regulation 292F(1), SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

[xi] Circular No. SEBI/HO/CFD/PoD-1/P/CIR/2022/120 dated September 19, 2022.

[xii] Regulation 91A, SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

[xiii] Regulation 91C, SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

[xiv] Circular No. SEBI/HO/CFD/PoD-1/P/CIR/2022/120 dated September 19, 2022.

[xv] Regulation 91D, SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

[xvi] Regulation 91E, SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

[xvii] Regulation 91F, SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

Author: Shubham Tibrewala, Associate (assisted by Shishank Shaw)

Disclaimer: The content of this article is intended to provide a general guide to the subject matter and that the same shall not be treated as legal advice. For any queries, the author can be reached at info@samistilegal.in